March 17, 2026

Employee Benefits Planning: Complete Guide & Examples

Employee benefits planning is one of the most consequential decisions an HR team makes each year. Get it right, and you attract top talent, reduce turnover, and build a culture people areproud to work in. Get it wrong, and you're left with a bloated budget, underused plans, compliance headaches - and a spreadsheet nightmare that keepsyour team up at night.

This guide walks you through everything: what employee benefits planning actually means, how to design a plan that fits your workforce, real-world examples by company size, and how to measure whether your plan is delivering results. Whether you're building benefits strategy from scratch or auditing what you already have, this is your starting point.

The stakes are enormous: employer-sponsored insurance currently covers 154 million non elderly Americans, making it the single largest source of health coverage in the United States (KFF, 2024 Employer Health Benefits Survey). And the costs keep climbing - average annual premiums reached $8,951 for single coverage and $25,572 for family coverage in 2024, increases of 6% and 7% respectively over the prior year.

What Is Employee Benefits Planning?

Employee benefits planning is the structured process of designing, budgeting, implementing, and managing an employee benefits program that supports both business goals and employee needs – and keeps supporting them as both the workforce and the regulatory environment change.

It includes:

• Health, dental, and vision coverage

• Retirement programs

• Voluntary and supplemental benefits

• Leave policies

• Wellness and mental health support

• Compliance oversight

• Ongoing cost analysis and vendor management

Benefits planning is not a one-time exercise. It’s a continuous cycle of evaluation, adjustment, and financial governance.

How Employee Benefit Planning Differs from Compensation

Compensation refers specifically to what employees are paid – base salary, bonuses, and commissions. Benefits planning covers everything else: health insurance, retirement savings, paid time off, disability coverage, wellness programs, andmore.

Together, compensation and benefits form an employee’s total rewards package. Benefits typically represent 25–40% of an employee’s total compensation cost – a significant investment that deserves the same strategic attention as salary.

According to the Bureau of Labor Statistics(ECEC, June 2025), benefits account for 29.8% of total compensation for private industry workers – that’s $13.58 per hour worked on top of $32.07 in wages.Health insurance alone accounts for 7.1% ($3.23/hr), making it the single largest benefits cost category.

Key distinction: Compensation is what you pay people to do their job. Benefits are what you offer to support their whole life.

That distinction is why candidates read the employment benefit plan before they negotiate salary – and that’s what drives long-term loyalty.

Why Employee Benefits Plans Matter

For large US employers, benefits planning directly impacts:

1. Talent Attraction & Retention

Strong benefits reduce turnover and increase offer acceptance rates.

The data backs this up: Bureau of LaborStatistics data reveals a striking correlation between benefits investment and employee retention.

2. Cost Control

Healthcare inflation continues to rise. Poor plan design leads to uncontrolled premium growth.

The KFF Employer Health Benefits Survey (2025) shows the scale of the challenge: the average annual family health premium reached $26,993 in 2025 – up from just $5,791 in 1999, a 366% increase in 26 years. This was the third consecutive year of 6%+ premium increases, the first time that has happened in two decades. In 2025, premium growth (6%) outpaced both general inflation (2.7%) and wage growth (4%), putting increasing pressure on benefits budgets.

3. Financial Risk Reduction

Incorrect carrier billing, missed terminations, and eligibility errors create premium leakage.

4. Compliance Protection

Regulations such as the Affordable Care Act (ACA), COBRA, ERISA, and state mandates add legal exposure.

5. Employee Experience

Benefits confusion or billing errors erode trust quickly.

A well-designed benefits plan improves workforce satisfaction. A poorly managed one creates operational chaos. That gap – between good employee benefit planning and reactive benefits administration – is where most of the financial and compliance risk lives.

Types of Employee Benefits

Benefits typically fall into three primary categories.

Core Benefits

These are foundational offerings expected by most US employees:

- Medical insurance (PPO, HMO, HDHP)

- Dental and vision

- 401(k) retirement plans

- Life insurance

- Short-term and long-term disability

- Paid time off (PTO)

For large employers, medical coverage is usually the single largest non-payroll expense.

According to the KFF 2025 survey, 61% of all firms offer health benefits – but that figure jumps to 98% among large firms (200+ workers). SHRM’s 2025 Employee Benefits Survey found that health-related benefits remain the #1 priority for employers for the fourth consecutive year, with 88% rating them “extremely” or “very important.”

Non-Traditional Benefits

These differentiate employers in competitive labor markets:

- Mental health programs

- Student loan assistance

- Flexible work arrangements

- Paid parental leave extensions

- Wellness stipends

Wellness programs – covering everything from meditation apps and mental health sessions to gym reimbursements and stress management coaching – have become the fastest-growing line item in mid-market benefits budgets, and among the highest-rated by employees under 40.

KFF (2025) reports that 83% of large firms and 56% of small firms now offer at least one wellness program (smoking cessation, weight management, or lifestyle coaching). According to SHRM, 75% of businesses with wellness programs report improved employee retention.

These benefits often cost less than core benefits but carry strong retention impact.

Voluntary & Supplemental Benefits

These are employee-paid or partially subsidized options:

- Critical illness insurance

- Accident insurance

- Hospital indemnity

- Pet insurance

- Legal services plans

They expand choice without significantly increasing employer costs – but they add reconciliation complexity.

How to Design a Powerful Employee Benefits Plan

Building a benefits plan that actually works requires more than copying last year’s lineup. Here’s a structured, eight-step process used by leading HR teams.

1. Define Business Goals

Start with the “why.” Are you trying to reduce turnover? Compete for talent in a tight market? Manage rising healthcare costs? Control benefits spend? Your objectives shape every downstream decision.

The business goal is what separates a strategic employee benefits plan from a list of coverages assembled at renewal. A startup focused on growth has different priorities than a 2,000-person enterprise managing cost containment.

2. Analyze Workforce Needs

Survey your employees. Understand what they actually value – not what you assume. Employee needs change as your workforce evolves – what worked two years ago may already be misaligned.

A benefits package built on assumptions rather than survey data is one of the most expensive guesses an HR team makes.

Demographics matter enormously. A workforce skewed toward younger employees may prioritize student loan repayment, mental health support, and flexibility delivered through wellness programs that address the whole person, not just the job. An older workforce may value long-term care insurance, robust retirement matching, and comprehensive health coverage.

3. Benchmark Industry Standards

Research what competitors and industry peers offer. Use data from SHRM Benefits Surveys, Willis Towers Watson, or industry benchmarking reports. Know where you stand – and where the gaps are. This is especially important if you’re competing for talent in high-demand roles.

4. Budget & Cost Modeling

Set a clear budget grounded in data. Benefits typically cost 25–40% of base salary. Model out different scenarios – what happens to cost if enrollment increases by 15%? What’s the impact of switching from a PPO to an HDHP? Finance and HR need to work together here.

Employee benefit plan design decisions made without financial modeling attached to them are guesses – and at benefits scale, guesses have dollar consequences.

Don’t forget to account for employer FICA contributions and administrative costs.

As context: KFF data shows that the average employer-sponsored family premium has grown from $5,791 in 1999 to $26,993 in 2025 – a 366% increase. Premium growth has outpaced both inflation and wage growth for three consecutive years.

5. Select Providers and Vendors

Evaluate carriers, third-party administrators (TPAs), and benefits platforms. Look beyond premium cost – consider network quality, member experience, claims processing speed, and administrative support.

For employers with 500+ employees, benefits administration technology matters as much as the plan design itself. Employee benefit plan design determines what you offer – technology determines whether what you offered is actually what gets delivered and billed correctly.

6. Design a Benefits Roadmap

Create a multi-year roadmap, not just an annual plan. Map out which benefits you’ll launch now, which you’ll phase in next year, and which are longer-term goals. This gives your team direction, helps with budgeting, and shows employees that you’re continuously investing in them.

7. Communicate to Employees

A great benefits package is worthless if employees don’t understand it. The most carefully designed benefits plan for employees delivers zero retention value if the people it was built for don’t know what it contains.

Studies consistently show that employees dramatically underestimate the dollar value of their benefits. Most employees think their benefits package is worth half of what the employer actually pays for it.

Use multiple channels – email, intranet, group meetings, and one-on-one sessions during open enrollment. Personalized annual benefits statements that show the true total compensation value are particularly effective.

8. Monitor and Iterate

Benefits planning is not a once-a-year event. Track utilization data monthly, re-survey employees annually, audit invoices and carrier billing regularly, and benchmark continuously. This is where many organizations fall short – and where significant savings and compliance risks hide.

A benefits plan for employees that is never measured is a financial commitment made without accountability.

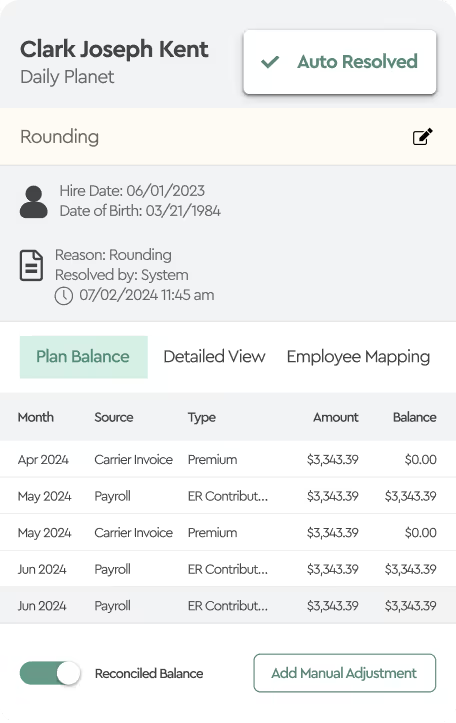

The hidden cost of “set it and forget it”: Most organizations review their benefits plan once a year during open enrollment – and then assume it runs itself. In reality, billing errors, eligibility discrepancies, and premium overcharges quietly accumulate month after month. Benefits reconciliation done manually in Excel is one of the most error-prone processes in HR operations.

Measuring The Effectiveness of an Employee Benefits Plan

If you can’t measure it, you can’t improve it. Effective benefits measurement goes beyond tracking premiums paid. Here are the metrics that matter:

Premium leakage – paying for employees who are ineligible, have already termed, or have incorrect dependent information – is one of the most common and costly measurement failures. Organizations lose an average of 1–3% of total benefits spend to preventable billing errors every year. At scale, that’s a significant dollar amount hiding in plain sight.

Employee Benefits Planning Design Strategies

The employee benefit plan strategies that work at 50 employees rarely scale to 500 – and what works at 500 rarely survives the complexity of 5,000.

Aligning Benefits with Company Culture

Your benefits package is a direct expression of your company’s values. A company that talks about work-life balance but offers no flexibility or mental health support sends a contradictory message. Align what you offer with what you stand for.

If innovation and autonomy are core values, offer benefits that support those – flexible schedules, learning stipends, and sabbaticals, wellness programs that support mental health and physical wellbeing, not just traditional HMO coverage.

Tailoring Plans to Different Employee Segments

A single plan rarely serves everyone equally well. The employee benefits plan that works for a 28-year-old in Austin is rarely the one that works for a 52-year-old plant manager in Ohio.

Consider segmenting by life stage, role, or geography. Offer a base plan plus optional add-ons. Some employers offer tiered plans – a standard option and an enhanced option – that let employees self-select based on their needs. This increases perceived value without proportionally increasing cost.

Research from SHRM, EY, and WorldatWork confirms that generational preferences vary significantly. Gen Z prioritizes mental health support, financial wellness programs, and digital-first healthcare. Millennials rank flexible work as their top priority (84% say it’s most important to job satisfaction), followed by student loan assistance and family-forming benefits. Gen X values 529 college savings, elder care support, and identity protection. Baby Boomers focus on robust 401(k) matching, retirement coaching, and comprehensive health coverage. One striking finding: 62% of employees across all generations say they would turn down a high-paying job if the benefits didn’t support their life outside of work.

Cost-Sharing vs. Premium Strategies

There’s no universally right answer on how much of the premium employees should pay. Too high, and employees resent the cost. Too low, and you’re leaving budget on the table that could fund other benefits.

The trend is toward transparent cost-sharing: show employees exactly what the employer contributes and let them choose coverage levels accordingly. HDHPs paired with employer-funded HSA contributions are one popular strategy for balancing cost and perceived value.

Compliance and Regulatory Considerations

Benefits are one of the most regulated areas of employment law. Key frameworks US employers must navigate include ERISA, the ACA, COBRA, FMLA, HIPAA, the ADA, and state-specific laws. Non-compliance isn’t just a legal risk – it’s a financial one.

For any employee benefits program operating at scale – across multiple states, multiple carriers, or multiple employer clients – compliance is not a checklist item. It is a continuous monitoring function that requires dedicated resources, documented processes, and regular legal review.

ERISA violations can result in personal liability for plan fiduciaries. Regular compliance audits and access to benefits legal counsel are non-negotiable for organizations managing plans at scale.

Employee Benefits Planning Examples

Small Business: 25-Person Marketing Agency

Unable to self-insure or offer rich benefits packages, small employers focus on high-impact, low-cost wins. This agency offers a group HDHP with a $500 employer HSA contribution, unlimited PTO, a $1,200 annual learning stipend, and access to a basic EAP. They don’t match 401(k) contributions yet, but offer the plan. Total cost: ~28% of payroll.

For a 25-person organization, this employee benefits plan delivers outsized perceived value relative to its actual cost. Result: strong retention driven by flexibility and development culture.

Mid-Size Tech Company: 350-Person SaaS Company

Competing for technical talent, this company offers a PPO and HDHP choice, 100% paid medical premiums for employees (50% for dependents), 4% 401(k) match, 16 weeks parental leave, $150/month wellness stipend, and a robust EAP with mental health sessions. They’ve added student loan repayment ($100/month) based on employee survey feedback. Total cost: ~35% of payroll.

Result: below-average turnover for their sector.

Large Enterprise: 3,000-Person Manufacturing Company

Benefits complexity scales significantly at this size. This company runs a self-insured health plan through a TPA, offers three plan tiers (HMO, PPO, HDHP+HSA), defined benefit pension for legacy employees plus 401(k) for new hires, and a comprehensive voluntary benefits marketplace.

They have a dedicated benefits team and use automated reconciliation software to manage monthly carrier billing across thousands of enrollees. For organizations at this scale, even small billing discrepancies can add up to significant annual overpayments if not identified and corrected.

Non-Profit Organization: 180-Person Social Services Non-Profit

Budget-constrained but mission-driven, this non-profit leverages Public Service Loan Forgiveness (PSLF) eligibility as a key recruiting tool, offers a generous PTO policy (25 days), strong mental health EAP coverage, and a SIMPLE IRA with a 3% match.

They don’t compete on salary – but their benefits and mission alignment drive loyalty. Their benefits package converts what would be a compensation disadvantage into a retention advantage. Total cost: ~26% of payroll.

Challenges in Employee Benefits Planning and How to Overcome Them

Even the most carefully designed employee benefits planning process runs into execution challenges. Here are the four most common – and how leading HR teams solve them.

Compliance Complexity

The problem: ERISA, ACA, COBRA, FMLA, state laws – the regulatory landscape is dense and constantly evolving. One missed notice or incorrect plan document can trigger significant penalties.

The fix: Build a compliance calendar and work with a benefits attorney on an annual plan review. Conduct independent annual reviews with legal counsel. Regular audits and proactive legal guidance help ensure your benefits program stays fully compliant while protecting fiduciaries from potential liability.

Low Employee Understanding and Utilization

The problem: Employees don’t fully understand the benefits they have – and therefore don’t use them, don’t appreciate them, and don’t factor them into their employment decisions.

The fix: Invest in benefits communication year-round, not just at open enrollment. Use plain language. Show total compensation value. Run “Benefits 101” sessions for new hires and annual refreshers for all staff.

Rising Healthcare Costs

The problem: Medical insurance premiums continue to climb annually, squeezing benefits budgets without delivering proportional value improvement.

The fix: Explore cost-containment strategies: self-insured plans for larger employers, reference-based pricing, direct primary care arrangements, and wellness programs that reduce utilization over time. HDHPs with HSAs can also shift cost responsibly without sacrificing coverage quality.

Tools and Platforms That Help with Employee Benefits Planning

Effective employee benefits planning involves multiple technology layers working in coordination – and the gaps between those layers are where most operational problems originate:

- Benefits Administration Platforms – manage enrollment and eligibility

- HRIS Systems – store workforce and payroll data

- Carrier Portals – provide billing and invoice data

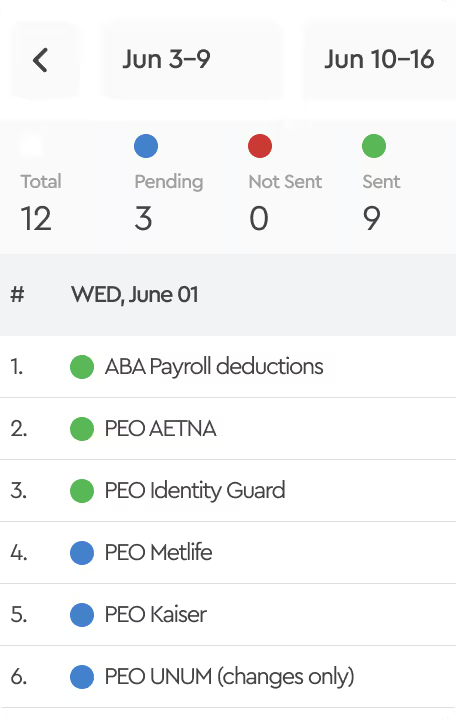

- Reconciliation & Audit Automation Software – this is where many organizations see the biggest operational gap

Manual reconciliation in Excel:

- Is time-consuming

- Increases audit risk

- Hides billing discrepancies

- Creates burnout for benefits teams

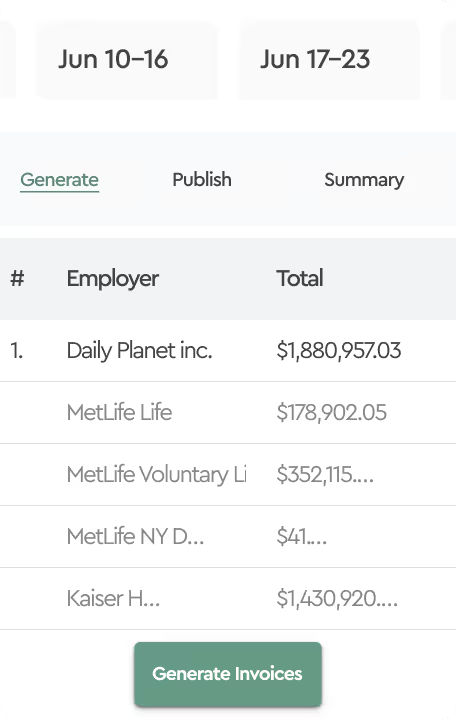

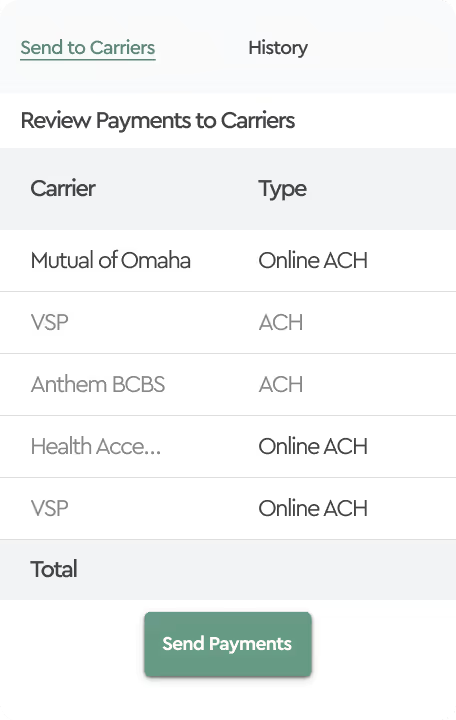

For large employers, automation platforms like Tabulera provide:

- Automated carrier invoice reconciliation

- EDI 834 connectivity – the standard electronic file that transmits enrollment changes directly to carriers, eliminating manual data entry errors

- Discrepancy reporting

- Premium leakage detection

The goal isn’t just efficiency – it’s financial accuracy and risk reduction.

Conclusion

Employee benefits planning is not a back-office administrative task. Done well, employee benefits planning is a strategic business function that directly affects your ability to attract and retain talent, manage costs, and stay compliant in an increasingly complex regulatory environment – and the organizations that treat it that way consistently outperform those that don’t.

The organizations that do this well share a few things in common: they start with employee data, not assumptions; they treat benefit plan design as a financial decision first and an HR decision second; they design for flexibility; they communicate clearly and consistently; and they treat plan monitoring as an ongoing discipline – not an annual afterthought.

For HR teams managing benefits at scale, the operational side of employee benefit planning matters just as much as the design. Billing errors, eligibility discrepancies, and manual reconciliation are real problems with real dollar consequences. The good news is that the tools to solve them exist – and implementing them is often one of the fastest wins available to a benefits team looking to demonstrate ROI.

If you’re managing benefits for 500+ employees, servicing multiple employer clients, or dealing with monthly reconciliation headaches, Tabulera is built for exactly that. Automated, accurate, and built by people who understand what’s at stake.

FAQs

What is the difference between employee benefits and perks?

Benefits are structured, often regulated components of total compensation – health insurance, retirement plans, paid leave, and disability coverage. Perks are informal extras that enhance the employee experience but aren’t tied to financial protection: free lunches, office ping pong tables, gym access, or flexible Fridays. Both matter to culture, but benefits carry legal, financial, and compliance weight that perks do not.

How much should a company budget for employee benefits?

A general benchmark is 25–40% of base salary per employee. According to the U.S. Bureau of Labor Statistics, benefits represent roughly one-third of total employer compensation costs in the U.S.

For employers with 500+ employees, benefits often represent one of the largest non-payroll operating expenses, making ongoing cost analysis and reconciliation essential.

What are common benefit plan design strategies?

The most commonly used strategies include: offering tiered plan options (e.g., HMO + PPO + HDHP) to let employees self-select; implementing consumer-directed health plans (CDHPs) paired with HSAs to control costs; using cafeteria-style or flex-credit plans that give employees a set budget to allocate across benefits; and segmenting benefits by employee population to ensure different needs are met across life stages and roles.

How do you conduct employee benefits analysis?

An effective benefits analysis has four components: utilization analysis (which benefits are actually being used and by whom); cost analysis (total spend, cost per employee, cost trend year-over-year); employee satisfaction measurement (survey data on perceived value and gaps); and competitive benchmarking (how your plan compares to industry peers). Add a billing and reconciliation audit to identify any premium leakage – it’s often the most immediately actionable finding in a benefits analysis.