May 21, 2026

Why Reconciliation Matters Even More When You're Self-Funded

I have a habit of checking the DOL’s website for public cases that are directly relevant to what we do at Tabulera. This week, this one caught my attention:

Dialysis Patient Who Lost Job Gets $200K in Treatments Covered. After a participant who was on dialysis lost his job, his former employer mistakenly kept him on their health plan for two extra months. When they realized their mistake, they canceled his coverage back to his job’s end date and said he had missed his chance to sign up for COBRA. The participant owed $200,000 in medical bills, as dialysis treatments are expensive and frequent.

However, due to the error, his company hadn’t sent a COBRA notice within the mandated timeline. With EBSA’s help, he was allowed to sign up, coverage was restored, and his claims were reprocessed.

He owed $200,000 in medical bills. EBSA stepped in, got his coverage restored, and his claims were reprocessed – a fantastic outcome!

That's the part that made the news. Here's the part that didn't.

If that employer had been reconciling their enrollment regularly, this never would have happened. A terminated employee staying active in the system for two months isn't a mystery – it's a data gap that a regular reconciliation catches.

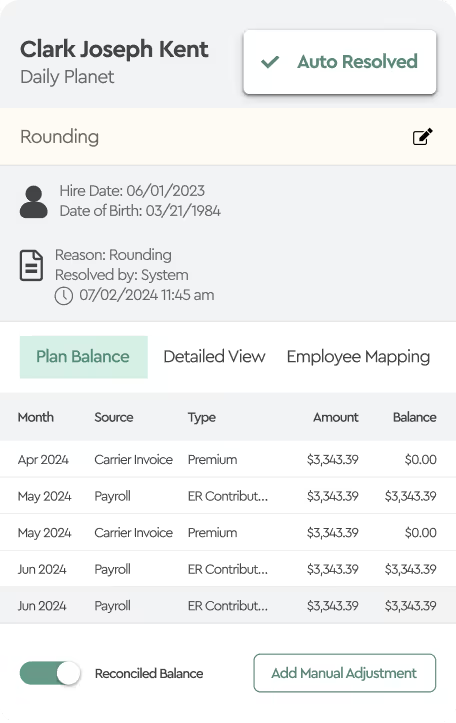

For smaller employers, Benefits Reconciliation typically gets treated like a fully insured concern – making sure the premiums you're paying to your carrier match what you're deducting from employee paychecks plus your employer contributions. Employer-side accounting.

Self-funded employee benefits are a different problem entirely. You're not matching deductions and contributions to a premium bill - you're funding claims as they come in. The question isn't whether the numbers balance. It's whether the right people are on your plan in the first place.

Cases like this rarely become public. This case became public because EBSA intervened. Most enrollment errors never make it to a federal agency – they just quietly cost the plan, or quietly cost the employee, and nobody ever connects the dots.

Self-Funded: A Different Category of Risk

The “dialysis case” got me thinking about the other side of the market – self-funded plans

To understand the scale, I pulled the Form 5500 for every Fortune 100 company – the 100 largest employers in the United States – to see how many of them are actually self-funded on medical.

Every single one.

In fully insured plans, the errors, we typically find, are between payroll deductions and what the carrier is billing – and the financial exposure is bounded. Our own internal research shows on average 1–2% of premium bills written off – terminated employees staying on the bill for months, rate mismatches, coverage discrepancies - most of it recoverable, when caught during the 60-90 day window.

With self-funded plans, the employer pays every claim directly. Stop-loss carriers can – and do – deny claims for members whose enrollment was never properly established, leaving the employer exposed above their deductible with no coverage.

In a fully insured plan, an enrollment error costs you a premium overpayment.

In a self-funded plan, it can cost you the actual cost of care – uncapped, and potentially uninsured.

How the Gap Happens

So how does enrollment data get out of sync in the first place?

Enrollment flows from the HRIS to the TPA – but verification means reconciling that data across three separate systems: your own records, the TPA's roster, and the stop-loss carrier's and network access invoice files. Most employers don't have a regular process for it.

The reasons data gets out of sync vary.

It can be an EDI feed running on a fixed schedule that suddenly stopped running one week and never caught a termination. Outdated, hardcoded file logic that could continue sending data for former employees to the TPA. Sometimes, an employee is deleted in the HRIS rather than properly terminated, so the downstream update never triggers. Other times, it's as simple as a duplicate plan record.

What matters is that in a self-funded plan, undetected means you're paying for it. Reconciliation catches it before the claim does.

Whether you're fully insured or self-funded, reconciliation belongs on the calendar – not on the crisis list. Modern tools make that realistic, even for lean teams.

Reconcile before it becomes a case study.