February 28, 2023

List Bills and Self Bills. Difference in the reconciliation process.

When it comes to managing an employee benefit plan, choosing the right billing method can make all the difference. This is where list-billing and self-billing come into play. List-billing involves the insurance carrier generating an invoice for premiums and sending it to the employer, while self-billing is when the employer creates and sends the invoice to the insurance carrier. Each method has its unique processes and reconciliation methods, and choosing the right one for your company can impact how you manage premiums and reconcile discrepancies. By understanding the differences and advantages of each method, you can make an informed decision on which billing method is best for your organization.

Employee benefit plans are an essential part of any organization. As an employer, you need to ensure that your employees receive the benefits they deserve, and one of the critical factors is paying the premiums on time. This is where list-billing and self-billing come into play.

What is List-Billing for an Employee Benefit Plan?

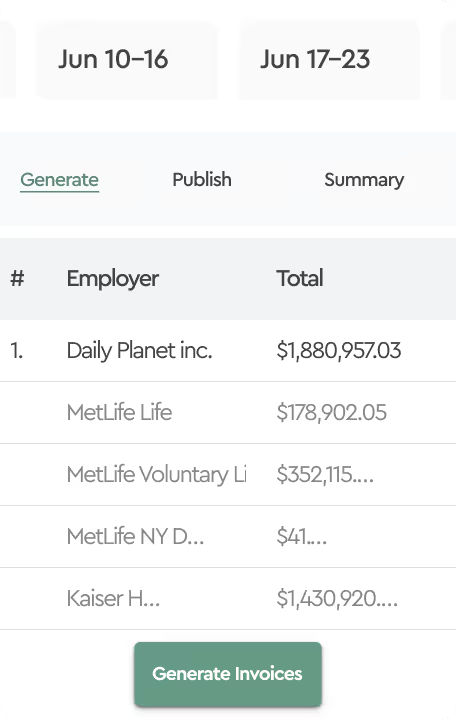

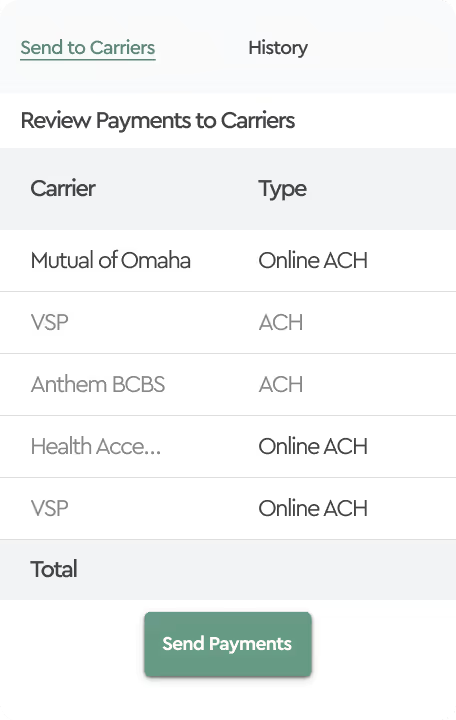

List-billing is a process where the insurance carrier generates an invoice for premiums and sends it to the employer. The data for the invoice is taken from the enrollment system, which may be manually entered into a carrier website, or larger employers may transmit the data directly to the carrier. The employer is responsible for paying the amount stated on the invoice to settle the transaction. Insurance companies usually publish the list-bill on their website.

What is Self-Billing for an Employee Benefit Plan?

Self-billing is a financial arrangement between the employer and the insurance carrier, where the employer creates an insurance premium invoice and sends it to the carrier along with the backup detail information. The data to create the invoice is usually derived from the employer's benefit enrollment or payroll system. The employer is then responsible for paying the amount stated on the invoice they created to settle the transaction.

What's the difference between Self and List Bills?

The main difference between self-billing and list-billing is who creates and sends the invoice. In self-billing, the employer creates and sends the invoice, while in list-billing, the insurance carrier creates and sends the invoice.

Comparing the Reconciliation Processes of List-Bills and Self-Bills for Employee Benefit Plans

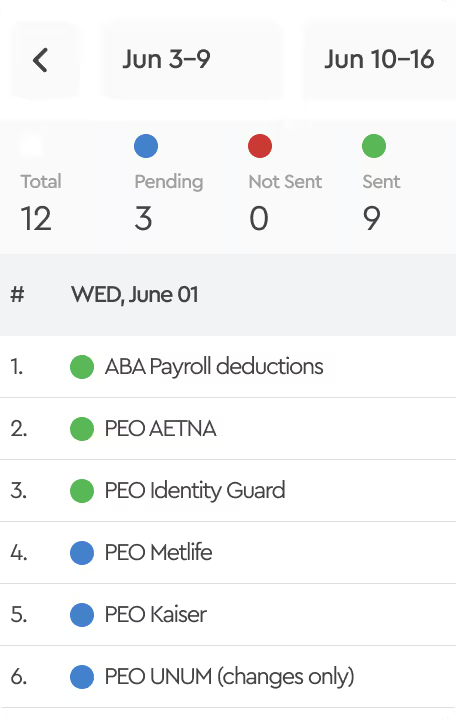

The reconciliation process also differs between list-billing and self-billing. With a list-bill, the employer needs to note any variances in timing that occur for new hires or terminations after the statement generation date and the enrollment and/or payroll system to ensure these are resolved on the following month's invoice. Differences in premiums between the enrollment and payroll systems may also occur due to carrier invoicing calculation errors or configuration of payroll deduction and/or plan enrollment premium tables.

While self-bills may eliminate enrollment and termination timing differences, they do not eliminate system configuration errors, such as lack of payroll deductions, leaves of absence, missed first or last deductions from partial months of employment. Moreover, self-bill programming or spreadsheets may introduce calculation errors given the complexity of eligibility and possible wash rule algorithms. The benefit or accounting team may be unaware that these errors even exist if premiums are not reconciled against a third-party invoice.

Conclusion

In conclusion, both list-billing and self-billing have their pros and cons. With list-billing, the carrier creates an invoice documenting what they believe the employer owes, and the employer can validate it against their own systems. With self-billing, the employer can eliminate timing differences, but it leaves them guessing what rates the carriers attach or when rate increases may take effect for their plans. Regardless of which billing method an employer chooses, monthly invoice auditing against their enrollment, payroll, and their invoices is a sure way to avoid surprises.